Digital Insurers Suffer Consecutive Losses [Talking Reporters_Finance_0409]

URL: https://www.youtube.com/watch?v=6mcqFrlcPLg

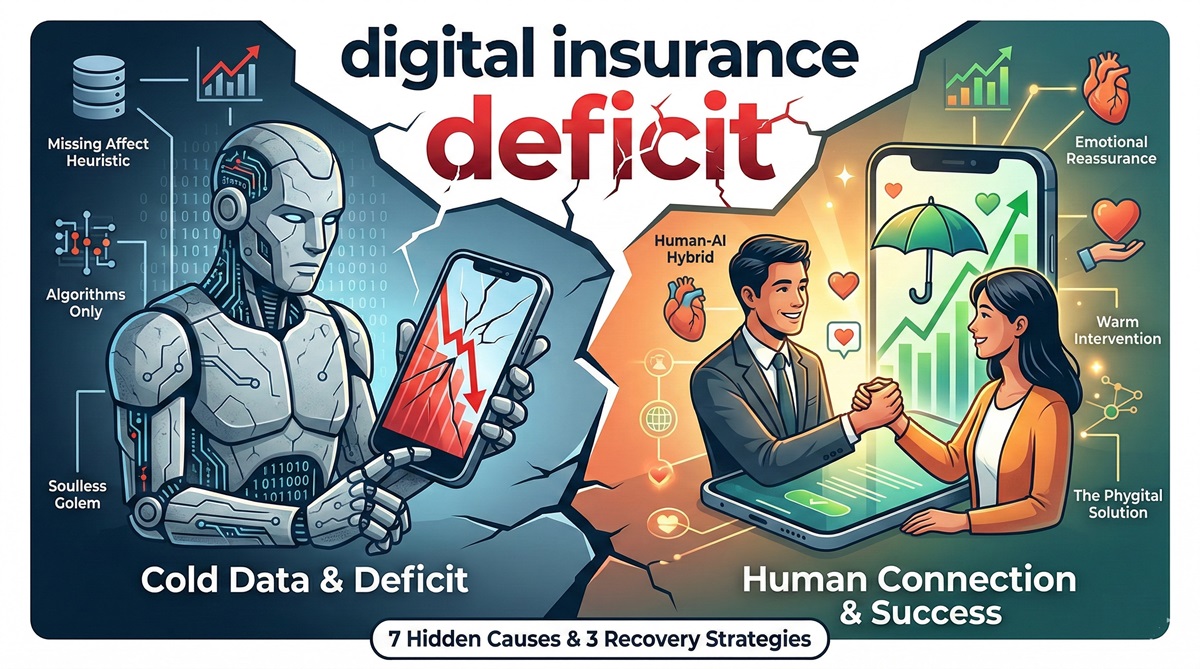

Looking at recent financial news, the most striking record is the painful news of the digital insurance deficit. The net loss of major domestic digital insurers reached 185.2 billion KRW last year, facing a severe situation. They attempted a perfect digital innovation where you can easily sign up with a single smartphone app, but in reality, turning a profit is not easy. Initially, they expected to make a profit by cutting costs through the elimination of offline channels. But what exactly went wrong? Today, beyond simple app usability issues, we will dig into this phenomenon from two deep perspectives: human psychology and the structure of macroeconomics.

The Continuous digital insurance deficit: Why Do We Buy Insurance from Agents Instead of Apps?

Insurance is a unique financial product that buys and sells invisible future risks. The first cause of the digital insurance deficit arises right here. Why do people insist on face-to-face consultations?

Missing the ‘Affect Heuristic’ and the digital insurance deficit

Traditional offline insurers pay quite high commissions to agents to attract customers. Digital insurers eliminated these commissions and promoted low-cost services. However, humans are governed by the ‘Affect Heuristic’ spoken of in behavioral economics.

- The Intersection of Fear and Relief: When facing the fear of disease or accidents, what a customer needs is not the cold information of a “3.5% chance of getting cancer.” It is the warm comfort and reassurance of a person saying, “If anything happens, I will help you until the end.”

- The Connection Apps Cannot Provide: Apps accurately calculate coverage details. However, they cannot transform the customer’s vague inner anxiety into relief.

- Reflecting on my past experience as an agent, the decisive factor for a customer to sign is not the product itself. You can only get their signature when the agent provides emotional connection and purchase confidence, showing they genuinely care.

Heidegger, the Limits of the Modern Golem, and the digital insurance deficit

Philosopher Martin Heidegger warned that technology reduces humans to mere data. A digital app stripped of emotion is like a ‘Golem,’ the soulless monster from Jewish legends. They increased sales by churning out micro non-life insurance like fire insurance for renters and travel insurance at an innovative speed. However, it was impossible from the start for a soulless algorithm to capture the deep hearts of consumers looking for a sturdy umbrella to stay with them for life, further deepening the digital insurance deficit.

Structural Limitations of the digital insurance deficit Failing to Withstand Macroeconomic Waves

The second cause that entrenches the digital insurance deficit comes from the difference in capital management weight classes. The real profit of the insurance business comes from ‘asset management,’ which rolls the collected premiums.

The Capital Dilemma in the digital insurance deficit

Excellent traditional companies accumulate massive liability reserves with customers’ money. They invest this money from a long-term perspective, much like the National Pension Service, to generate returns.

Exchange Rate Walls Deepening the digital insurance deficit

To maximize profits, they invest in US stocks or dollar-based excellent overseas assets. To prevent the inevitable exchange rate fluctuation risks, they use sophisticated currency hedging techniques. Through this, they generate stable profits and pay dividends to shareholders.

The Micro-Insurance Trap Accelerating the digital insurance deficit

However, the one-month or one-year micro-insurances mainly sold by digital insurers cannot create such a massive reservoir of capital. Because the incoming money is small, they simply lack the capacity to build an asset management portfolio to respond to the global macro environment.

3 Hybrid Strategies for 2026 to Escape the digital insurance deficit

So, should digital insurers close their businesses? No. To escape the digital insurance deficit, a strategy combining digital convenience with offline human warmth is absolutely necessary. I have thought of these methods.

- Building a Hyper-connected Hybrid Channel: Leave simple information searches to the app, but for moments of complex decisions like long-term health/pension insurance, a seamless system must be introduced where video consultations or professional human advisors can intervene immediately.

- Data-Driven Hyper-personalized Emotional Messages: Instead of mechanical notifications, warm copywriting that deeply sympathizes with the customer’s lifestyle (marriage, job change, etc.) by analyzing MyData must be integrated throughout the UI. It is the work of replacing cold statistics with warm comfort.

- Modularizing Long-term Coverage Centered on Profitability: Mini-insurances that are easy to cancel at any time cannot withstand the shocks of exchange rates or macroeconomics. After building solid trust through human counseling, the constitution must be completely improved with a flexible, high-return long-term insurance lineup where customers can assemble only the coverage they need like Lego blocks.

Time to Breathe Warmth into Cold Data to Overcome the digital insurance deficit

The massive loss of 185.2 billion KRW is not a simple failure of a business model. It is a painful market warning that algorithms cannot completely replace the essence of finance, which is trust between people. Now is the time to break out of the shell of the soulless Golem and build strong stamina to ride the waves of macroeconomics. Only when we completely understand the affect heuristic and breathe human warmth into the system can we escape the long swamp of the digital insurance deficit and achieve true financial innovation.

“Insurance is not a business of reason selling statistics, but a business of emotion calming anxiety. To overcome the waves of exchange rates and macroeconomics, a high-return long-term product strategy (‘Phygital’) combined with ‘warm human intervention’ beyond short-term micro-products is the only solution.”